- Personal

- Membership

- Membership

- Rates & Fees

- Checking

- Checking

- Personal Loans

- Personal Loans

- Wealth Management

- Investment Services

- Financial Advisors

- Resource Center

- Business

February 21, 2025

Understanding Compound Interest: Making Time Work for You

Even if your retirement is still decades away, saving should be a priority. Why? When it comes to maximizing your dollar, time really is money. That’s why you need to understand compound interest.

Make the most of compound interest

You’ve likely heard us say it before — start saving for retirement as early as possible — but you may not have considered the math behind the savings equation. The real magic is compound interest. How does it work?

- Save money in a diverse portfolio that earns interest.

- Watch as your new higher total earns even more interest.

- Rinse and repeat. As your balance grows, your interest compounds, allowing you to earn even more, and this continues over and over.

That’s the bottom line — and why it’s so important to save early and often. There’s more time for compounding to work its magic.

Understand the value of time

Consider two simple scenarios to help you visualize the impact of time on your savings outcome.1 Both scenarios assume the same initial contribution, monthly contribution and interest rate.2 The only difference? Time.

1Figures quoted are for illustrative purposes only and are not necessarily indicative of past or future results of any specific investment. They may or may not include consideration of the time value of money, inflation, fluctuation in principal or, in many instances, taxes.

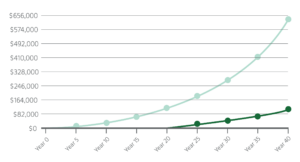

Scenario 1: Saving for 20 years

If you start with just $1,000 and save $50 per week ($200 monthly) for 20 years, you end up with about $114,500. While this is meaningfully better than not saving at all, this amount probably won’t stretch through a long retirement and may leave you with an expenses gap.Scenario 2: Saving for 40 years

Let’s say you start with the same initial amount of $1,000 and save the same $50 per week, but you begin saving earlier — with 40 years to spare until your goal retirement age. Now, you may end up with about $643,500. The extra 20 years of compounding more than quintuples your total and provides a much more comfortable figure to support you during retirement.Plus, this illustration doesn’t take into account that as a person’s career progresses, they’re typically able to increase the amount they’re contributing to retirement savings, which means even more compounding to take advantage of. To calculate savings outcomes based on different interest rates and contributions over time, you can use the U.S. Securities and Exchange Commission’s compound interest calculator.

Our advice? Start early, save often.

Imagine what compounding interest could do for you. Even small monthly contributions will add up. Disciplined, consistent saving habits are the key to safeguarding your financial future.

2The graph shows an estimate of how much your initial savings plus monthly contributions can grow over time, assuming an 8% interest rate and annual compounding. Remember that adjustments in any of those variables will change the outcome.

Posted In: